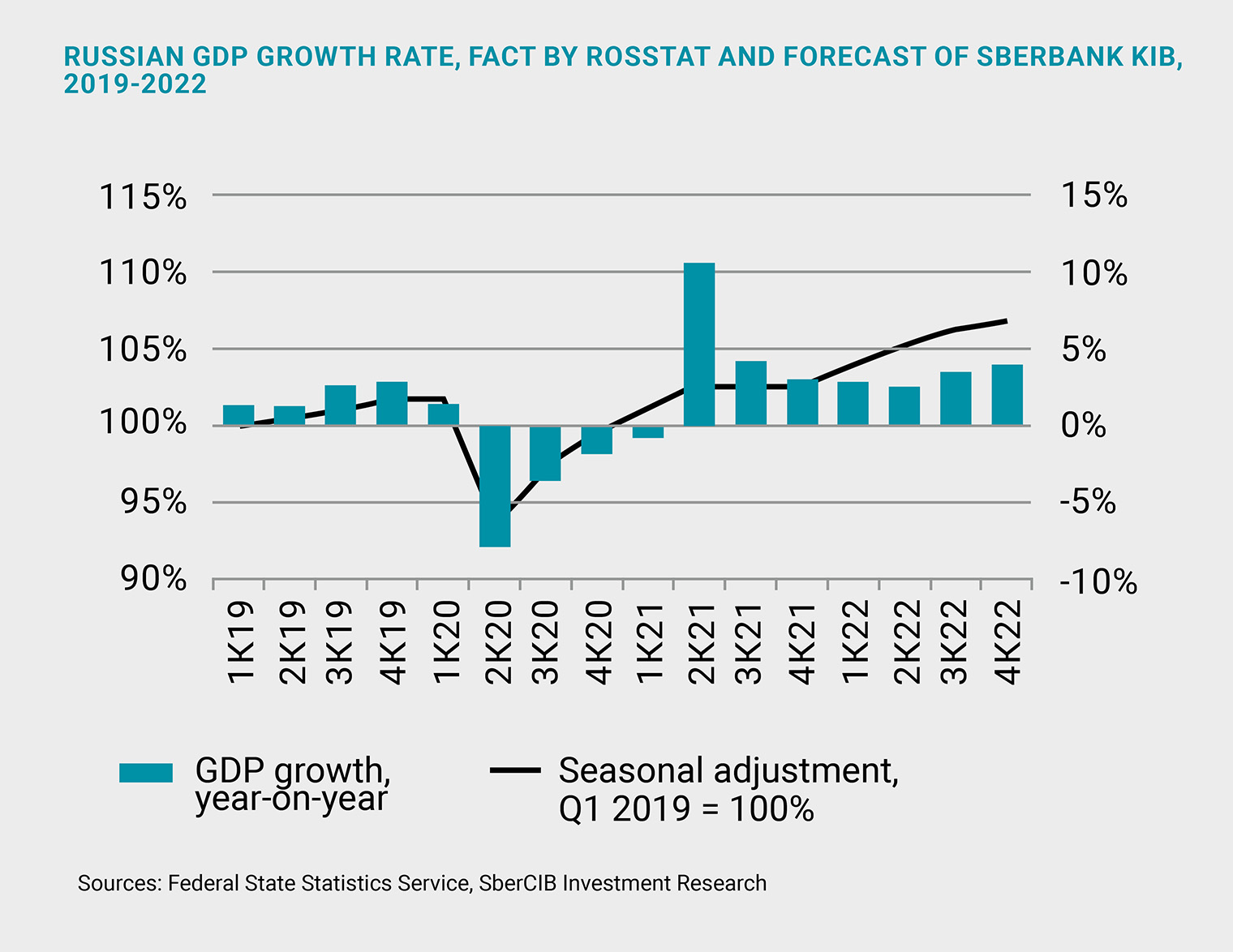

The economy has recovered to pre-COVID levels and is gradually slowing down. The drivers of recovery have fizzled out, monetary policy is being tightened, and lockdown is making occasional comebacks. According to preliminary estimates, GDP grew 4.3% year-on-year in Q3 2021 and was up 4.6% year-to-date. Russia’s GDP is expected to slow to 2.5% next year and may further decline to 1.5%–2%. This may be driven by factors such as demography (a reduced workforce), lack of foreign investment, and structural problems.

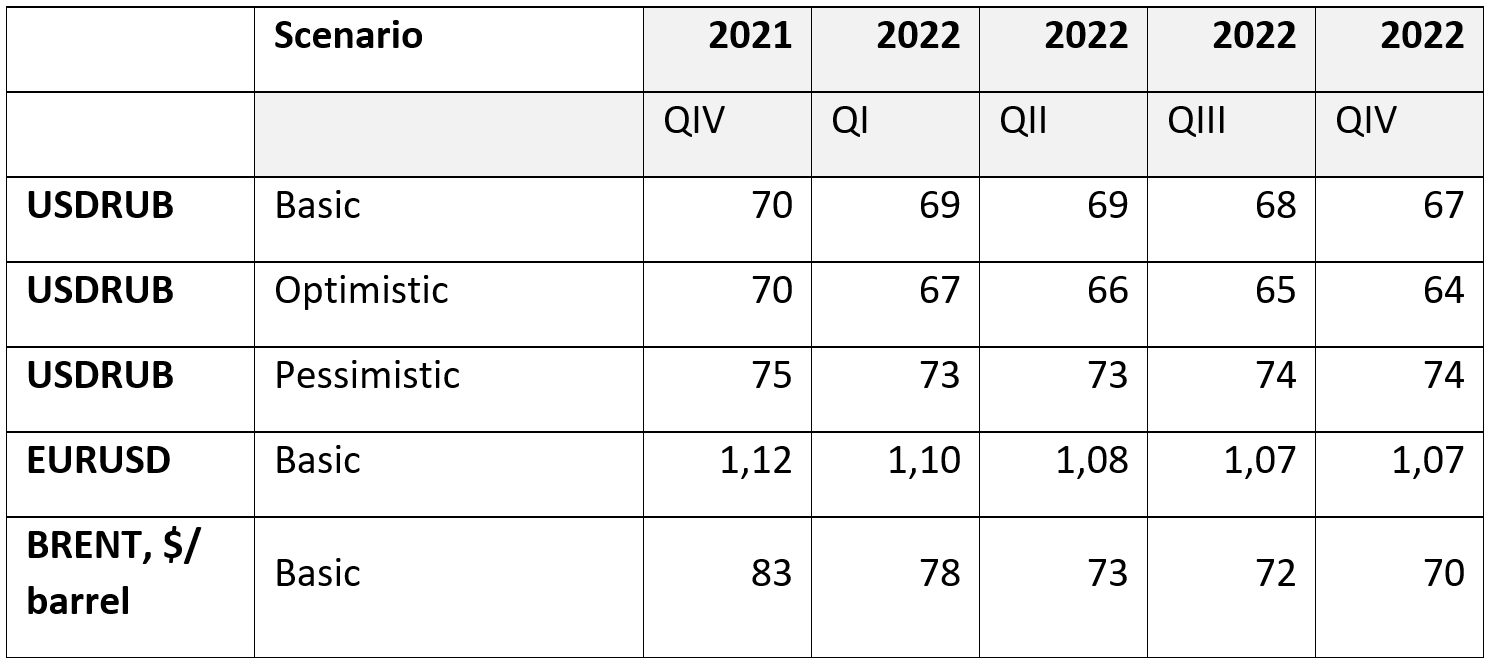

In the base case scenario, the rouble will strengthen moderately against the US dollar and more significantly against the euro. Oil prices will remain high due to the extension of the OPEC+ deal and low inventories at the end of 2021.

Domestic factors

"+" National Wealth Fund investments. The investments of Russia’s National Wealth Fund (NWF) are capped at 7% of GDP, and the NWF is currently worth 12% of GDP. On 19 November, the Federation Council approved an increase in the threshold for the NWF’s liquid assets from 7% to 10% of GDP. Nevertheless, the NWF may be used to finance selected self-funding infrastructure projects in 2022 to the tune of up to RUB 2.5 trillion.

"–" Annualised inflation accelerated to 8.1% in October, its highest since February 2016 (in January 2016, the average Brent price sank to USD 30.7 per barrel amid a slowing global economy and the peak shale production). Rising food prices were the largest contributor to inflation in August–October. Inflation in October hit the highest for this month since 2007. A smaller wheat harvest had a negative impact on agricultural production.

"–" At the end of October, the Bank of Russia raised its key rate by a staggering 75 bps to 7.5%. Market participants clearly expect the Bank of Russia to announce a further rate hike at its next meeting, given the weekly inflation rates and the regulator’s statements about possible further rate increases to address inflation expectations. The Bank’s forecast does not rule out a rate hike of 100 bps in December, with the rate peaking at 9% next year.

"–" OFZ. In October, non-residents’ investments decreased by RUB 55.7 billion, with the last week seeing the biggest outflow (RUB 81 billion) on the back of rising rouble interest rates. OFZ sales by non-resident investors hit an 18-month high in the last week of October – the highest since March 2020 when foreign investors fled OFZs at the onset of the pandemic.

CIB forecasts for the end of the period:

External factors

"+" High gas prices will bring in tens of billions of extra dollars to Russia’s currency market, bolstering the rouble. Next year, Russia’s extra revenue from gas sales may vary from USD 20 billion to 100 billion, with the gas price in Europe ranging from USD 375 to 1,000 per thousand cubic metres, respectively. Windfall profits from high gas prices are not covered by the Russian Finance Ministry’s budgetary rule, unlike those from high oil prices. The extra inflow of USD 20–100 billion may thus result in the Russian rouble strengthening to RUB 67 per USD next year. The situation in the gas market is a mixed picture: the gas rally to USD 1,300 per thousand cubic metres will reverse if the issues surrounding Nord Stream 2’s certification find a constructive resolution.

"+" Planned federal investment in the US infrastructure and its impact on the country’s economic growth. The US Senate gave bipartisan approval to a near USD 1.2 trillion infrastructure plan (IIJA), the positive impact of which on GDP will peak in 2024.

"+" The European Central Bank will soften its monetary policy, and the euro will weaken against the US dollar amid a growing gap between real yields of US and European government bonds, all while high energy prices negatively impact the trade balance.

"–" High inflation is global. Core inflation is rising around the world. Commodity prices are at five-year highs. Metals, grains, and fertilisers are up 30% year-to-date. Freight rates are growing as well. Some Asian electronics manufacturers have an 18-month waiting list for new orders. There are concerns about manufacturers in China raising their prices. The US annualised inflation hit a 31-year high of 6.2% in October. In Germany, annualised inflation was 4.5% in October, the highest since 1993.

"–" During the pandemic, consumers in developed economies accumulated USD 2 trillion in their current and savings accounts (mostly high net-worth individuals). Against the threat of inflation, people may start spending these savings.

"–" The US Federal Reserve (Fed) will tighten its monetary policy amid high inflation. The cumulative 10-year gap of the US inflation rate to the Fed’s target has narrowed by 3%, and is now less than 1.5%. The US economy surpassed pre-COVID levels in the second quarter of this year. Unemployment in the US fell to 4.6% in October, the lowest since March 2020 – close to the natural rate. Despite a widespread shortage of workers, it is still above the pre-COVID level of 3.5%. The pandemic has led to drastic shifts in the labour market, with a growing demand for secondary sector jobs, while most job losses are concentrated in travel, tourism, and outdoor recreation. Concerns about inflation lingering on if the commodity rally continues will result in US consumers starting to spend their excess savings, which may make the already high inflation worse. At the moment, the Fed expects significant rate hikes in 2023 and 2024, with the market expecting stronger growth.

"–" The difference in the real yields of bonds in the US and other countries will continue to narrow, with the dollar appreciating further.

"–" Oil. At the end of November, negotiations with Iran resumed, as the market entered a period of seasonal decline in demand amid further supply growth. The market is anticipating that the US and China will tap into their strategic reserves. The price growth potential of oil as a substitute for gas is gradually being exhausted. Gas-fired electricity generation cannot be entirely replaced with diesel and fuel oil. The additional demand for oil during winter season may hit 500–700 thousand barrels per day (2–3 million per month). Most of the year, oil prices have been steadily going up, driven by market conditions.

Comments (0)