2022 will be the year of the Tiger, according to the Chinese zodiac calendar. Astrologers assure us that the year will be a rollercoaster ride of excitement and events. Unlike astrologers, analysts do not look to the stars or read horoscopes – they rely on numbers and facts. This time, however, it seems that SIBUR’s experts largely agree with the astrological predictions. 2022 is going to be a challenging year. To prepare yourself as fully as you can and trim your sails to the wind, study our detailed analysis of the oil and petrochemical market below.

Prices on the uptrend

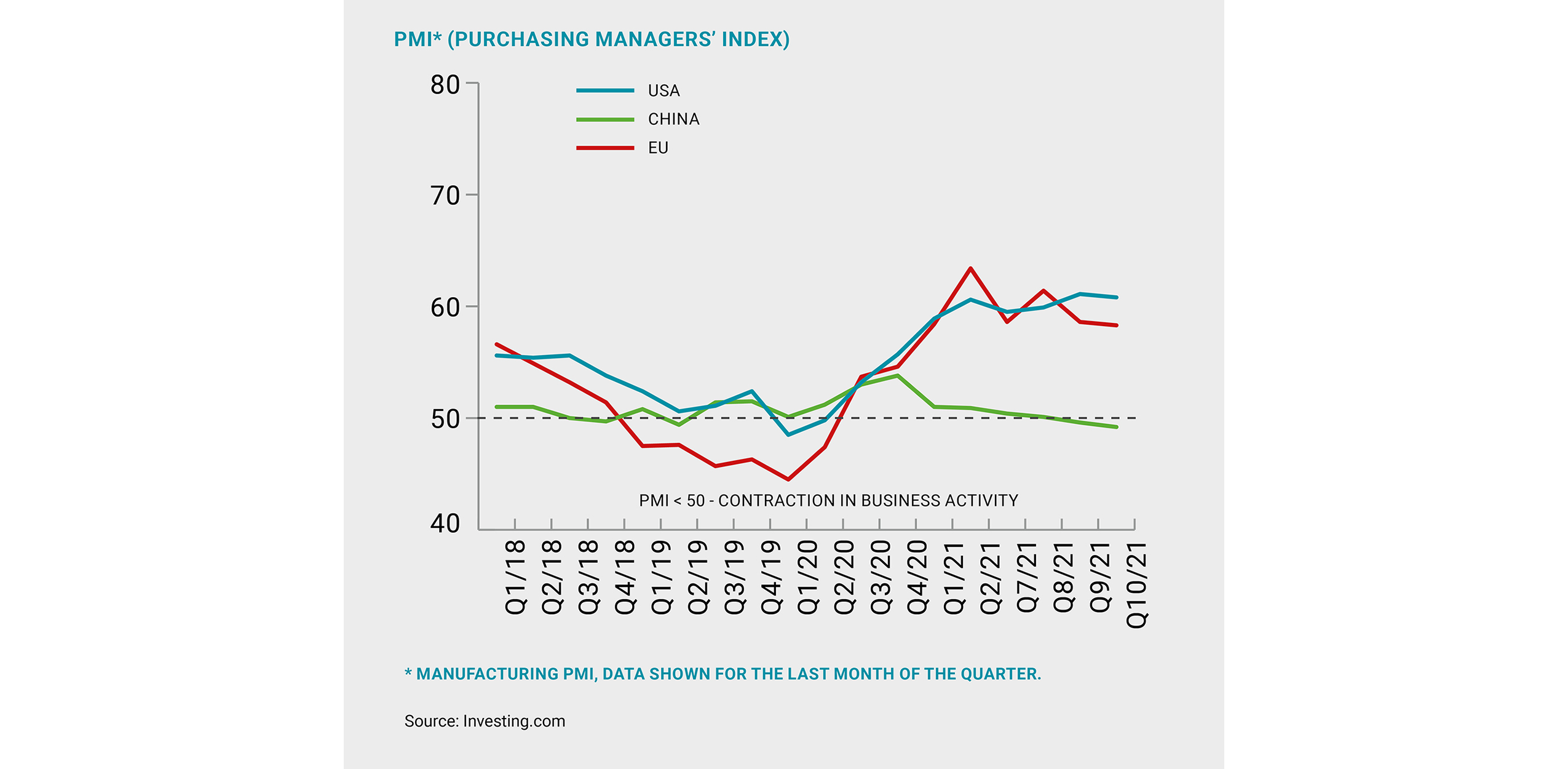

Mounting consumer inflation is the key highlight of the outgoing year, and it will most likely continue into the next one. The USA was among the hardest hit, with inflation rising to 6.2% in November, a 30-year high. In the Eurozone, the figure was 4.1%, a level last seen in 2008. Although the US and EU manufacturing PMI sits around 60, this is not enough to meet end-consumer demand and slow inflation. In Russia, inflation also continued to rise and reached 8.13%, its highest since 2016.

THE GLOBAL SURGE IN CONSUMER PRICES ACROSS ALL MARKETS HAS BEEN DRIVEN BY A NUMBER OF KEY FACTORS, IN PARTICULAR THE RISING COST OF ENERGY

The global surge in consumer prices across all markets has been driven by a number of key factors, in particular the rising cost of energy (oil, gas, and coal) globally amid increased consumption coupled with supply constraints. The prices for homes, food, and cars have also risen.

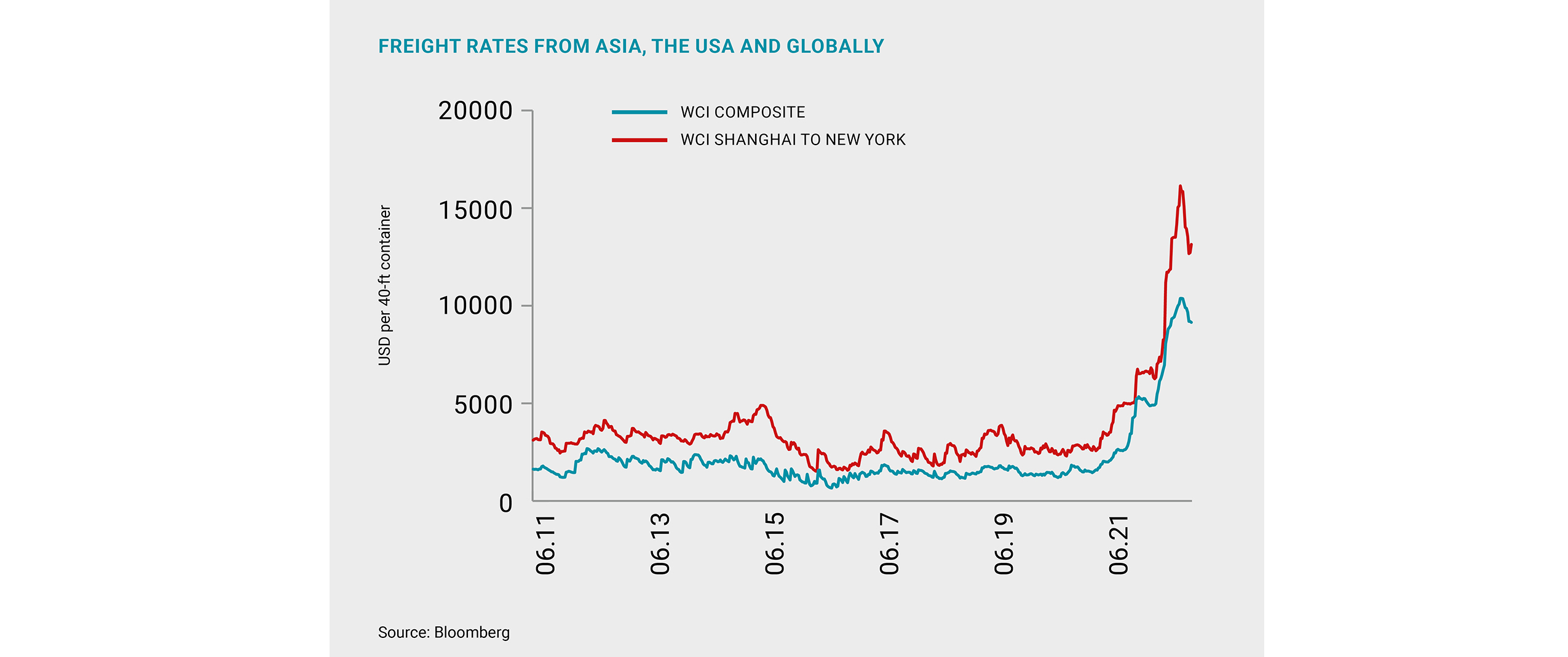

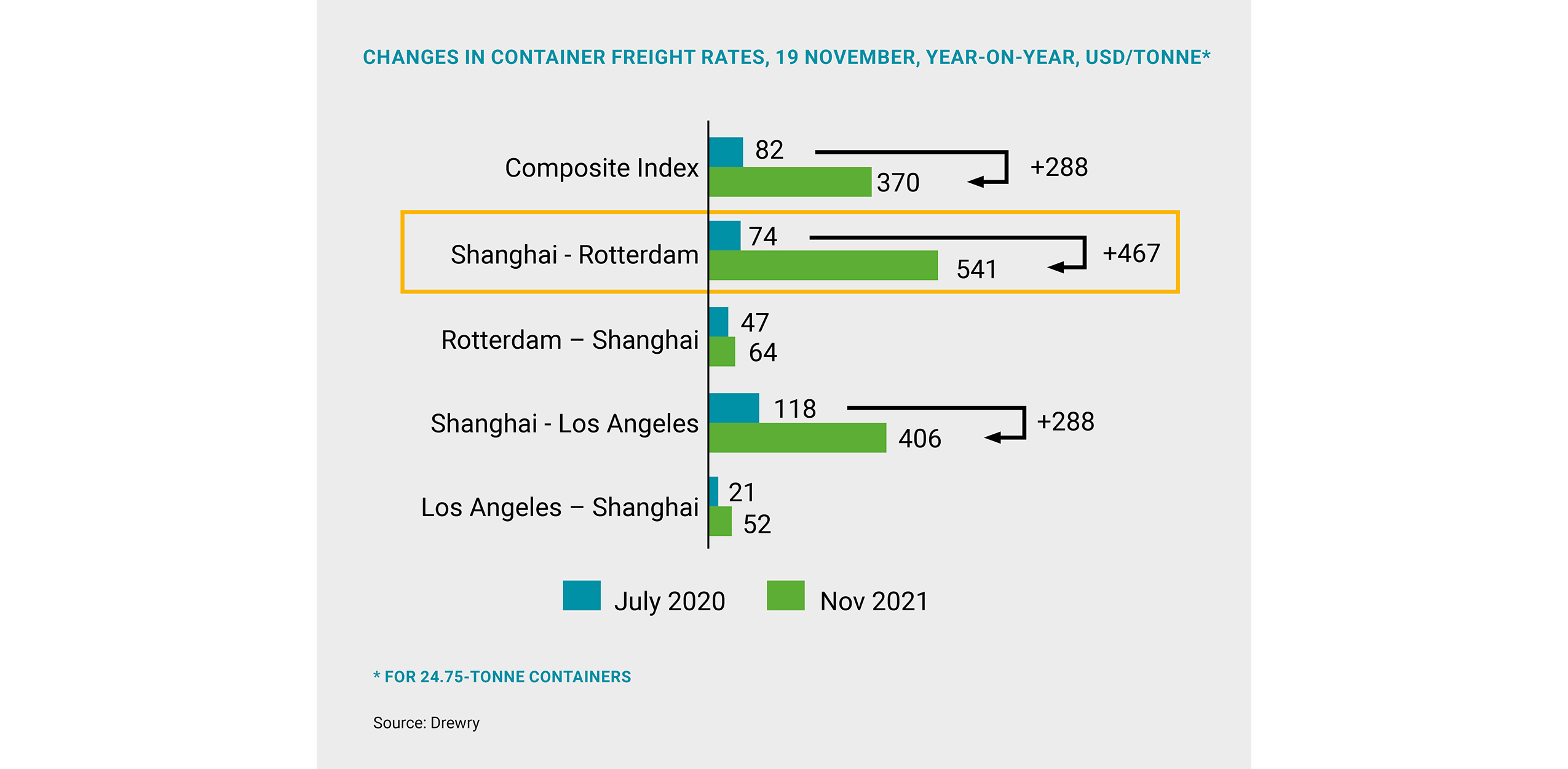

Also weighing on prices are the persistently high container shipping rates, which cause constraints in global trade and further tighten market supply. For example, shipping rates from China to the USA rose until mid-September to exceed USD 16,000 per 40-foot container, after which spot prices dropped to USD 13,100 in mid-November. Analysts estimate that the market will remain tight throughout 2022, gradually debottlenecking by early 2023 as new ships and containers are built. Another factor that may ease logistics costs could be a potential reduction in demand for end products amid high inflation.

Interestingly, less developed countries do not have particular problems with high inflation. This is due to the slower recovery of their economies from the pandemic and the resulting slow growth in demand for consumer goods and services.

In China, the trends are reversed: PMI and inflation are declining. This led to a GDP growth of 4.9% in the third quarter vs the expected 5.2%. Meanwhile, consumer inflation rose sharply to 1.5% in October, with producer price inflation at 13.5%, a 26-year high.

The slowdown in economic activity in China is due, among other reasons, to the reduction of stimulus packages and the power crunch. China is facing energy shortages due to insufficient coal supply and its Dual Control policy, which regulates energy consumption across provinces and the nation as a whole. Note that the Dual Control policy is one of the mechanisms for achieving China’s environmental targets, which include a 13.5% cut in energy consumption per unit of GDP by 2025.

UNCERTAINTY IN THE OIL MARKET IS PRIMARILY FUELLED BY THE NEGOTIATIONS BETWEEN THE USA AND IRAN ON ITS NUCLEAR PROGRAMME; THE TALKS ARE RAISING DOUBTS THAT US SANCTIONS WILL BE LIFTED ANY TIME SOON

Oil: endless shortages?

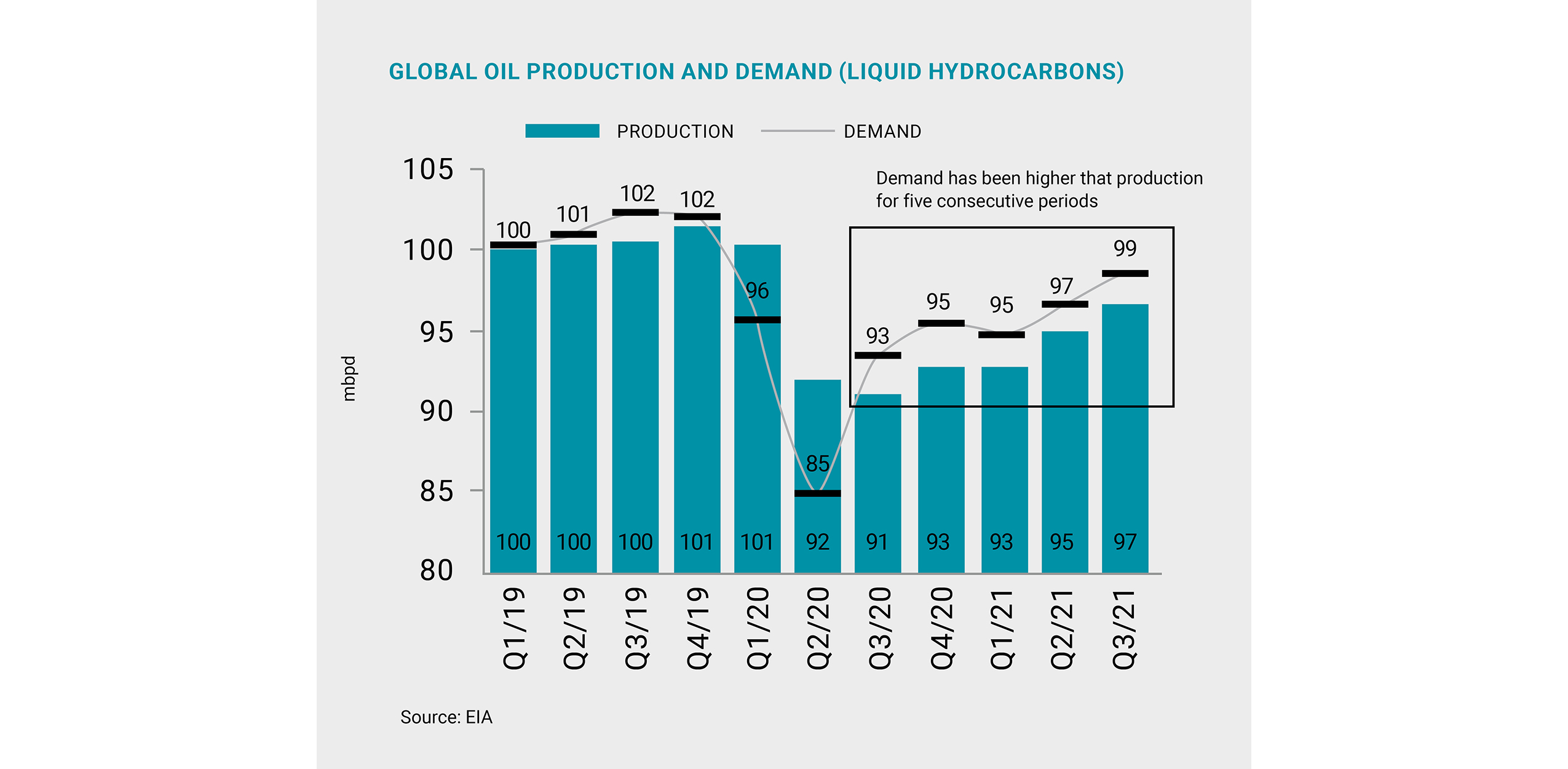

In the third quarter, the average Brent price grew 7% quarter-on-quarter to USD 73.5 per barrel. The increase was due to demand exceeding supply by 2 mbpd (Q3 average, EIA estimate) on the back of the OPEC+ policy of not increasing quotas in September and August despite strong consumption growth. As a result, oil shortages have persisted in the market for five consecutive quarters. In addition, there were no significant production increases in non-OPEC+ countries, including shale oil producers in the USA.

US oil production was limited due to Hurricane Ida, which occurred in late August and led to a reduction in the country’s strategic oil reserves. In the third quarter, the USA produced 11.1 mbpd of oil (down 0.2 mbpd quarter-on-quarter). Drilling and well completion rates are recovering, but the current rate of commissioning new wells will only keep production at current levels. It is clear that to grow production in 2022, companies will have to seriously step up new well CAPEX. For example, private producers, which account for a third of US oil output, have reached well drilling rates of 75% of the 2019 average, while large public companies only hit 50%.

Oil supply may continue to be constrained due to some OPEC+ members not being able to ramp up their production to meet the quotas. Uncertainty in the oil market is primarily fuelled by the negotiations between the USA and Iran on its nuclear programme; the talks are raising doubts that US sanctions curbing Iranian oil exports will be lifted any time soon.

THE REGIONAL PROFILES OF SUPPLY AND DEMAND FOR PETROCHEMICAL PRODUCTS HAVE LED TO OPPOSITE TRENDS FOR THE IPEX PRICE INDEX. IN THE USA, PRICES CONTINUED TO RISE; IN ASIA THEY REMAINED STABLE; BUT IN EUROPE, THEY WERE FALLING

IPEX: Opposite trends

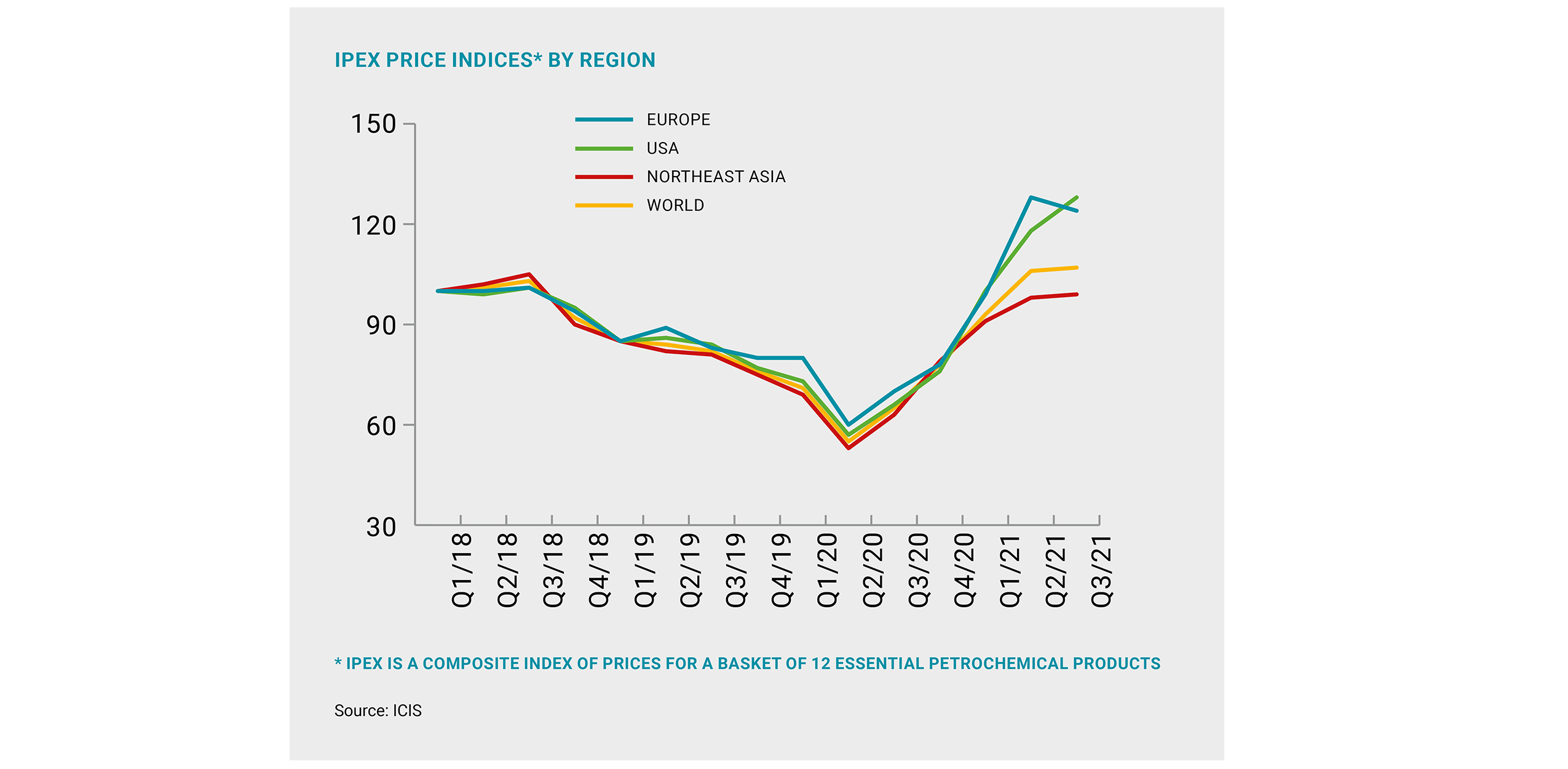

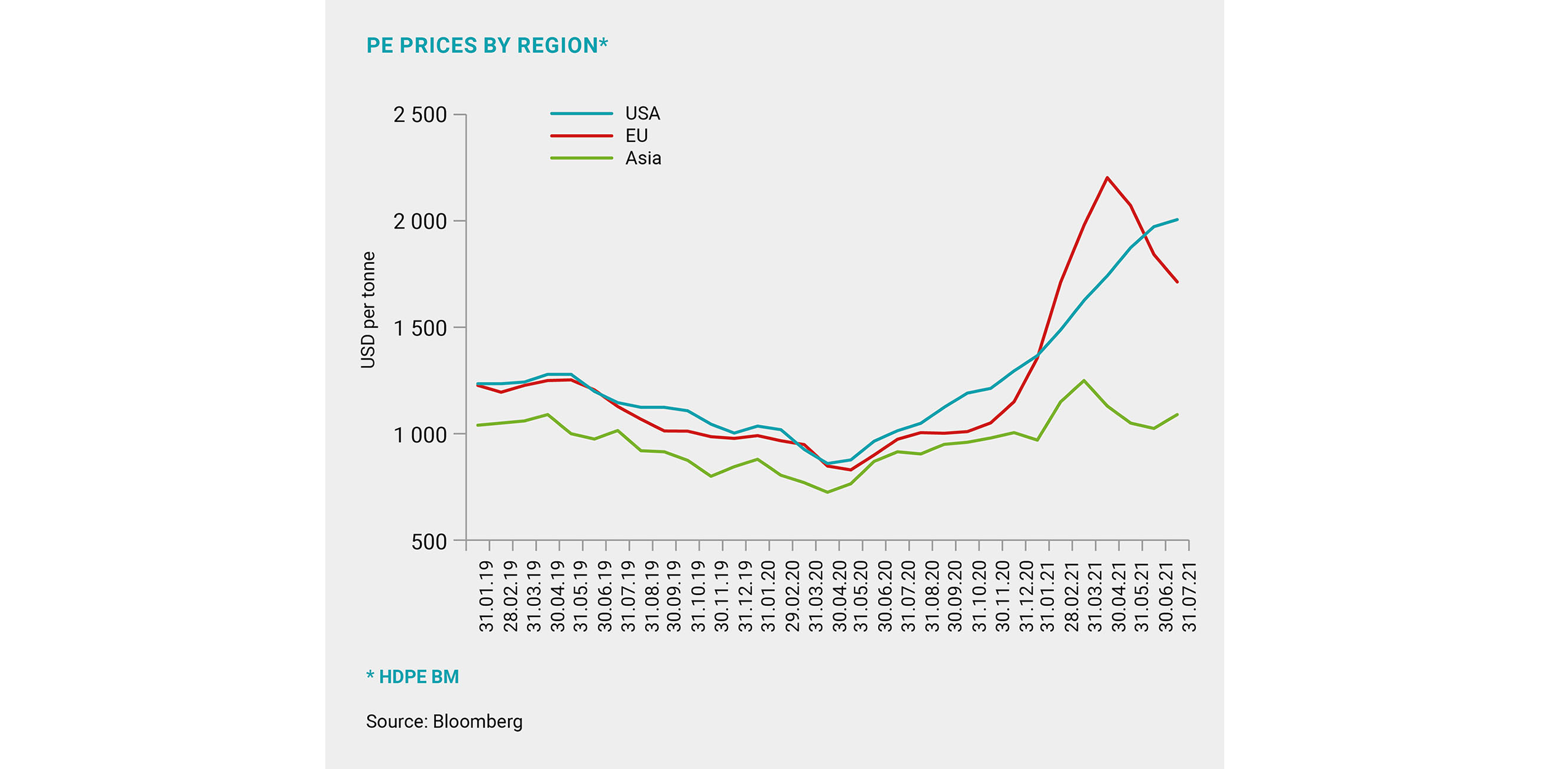

The regional profiles of supply and demand for petrochemical products have led to opposite trends for the IPEX price index. In the USA, prices continued to rise; in Asia they remained stable; but in Europe, they were falling. The global price index has grown by 14 p.p. year-to-date, with the USA posting the highest growth over this period. The significant gap in the index between regions can be explained by regional product mix profiles and high transportation costs, which prevent these arbitrage windows from being quickly addressed.

For example, the cost of shipping polymers from China to Europe rose from USD 90 per tonne in January 2021 to USD 540 per tonne in mid-November, peaking in mid-October at USD 590 per tonne. As logistical issues get resolved, prices in these regions will start to decline and the price differential will fall to historical levels. Prices by product during the third quarter also showed opposite trends as PP and rubbers posted growth, while prices for PE and PET were down.

THERE HAVE BEEN SEVERAL MAJOR CHANGES IN THE POLYETHYLENE (PE) MARKET. ONE OF THE KEY DEVELOPMENTS WAS THE IMPACT OF CHINA’S DUAL CONTROL POLICY, WHICH HAS LED TO EXPECTATIONS OF LOCAL POLYMER SHORTAGES WHILE SUPPORTING PE PRICES

PE: ambitious plans

There have been several major changes in the polyethylene (PE) market. One of the key developments was the impact of China’s Dual Control policy, which has led to expectations of local polymer shortages while supporting PE prices. Prices in China’s domestic market have accelerated since mid-September.

China keeps launching new projects, ramping up its domestic output, and reducing imports. According to PlasticHelper, China imported 11.76 million tonnes of PE in 9M 2021, down 17% year-on-year.

China also continues to build up its PE exports, which are insignificant compared to imports, but show record growth. From January to September 2021, PE exports from China increased by 113% to 416,000 tonnes.

As for the US market, the key event affecting the polyolefin market was Hurricane Ida, which led to the temporary shutdown of a number of facilities, translating to lower utilisation and production. Ida was many times less destructive than Winter Storm Uri, which happened in February. Supply shortages caused by natural disasters affected PE trade flows. In the first nine months of 2021, US PE exports fell 19% year-on-year according to Mrcplast. This, in turn, supported prices in other regions of the world.

CHINESE PP PRODUCTION – SUPPORTED BY GREENFIELD PROJECTS – IS GROWING IN THE FACE OF TEMPORARY SHUTDOWNS AND LOWER UTILISATION AT SOME PDH (PROPANE DEHYDROGENATION) PROJECTS DUE TO DECLINING MARGINS

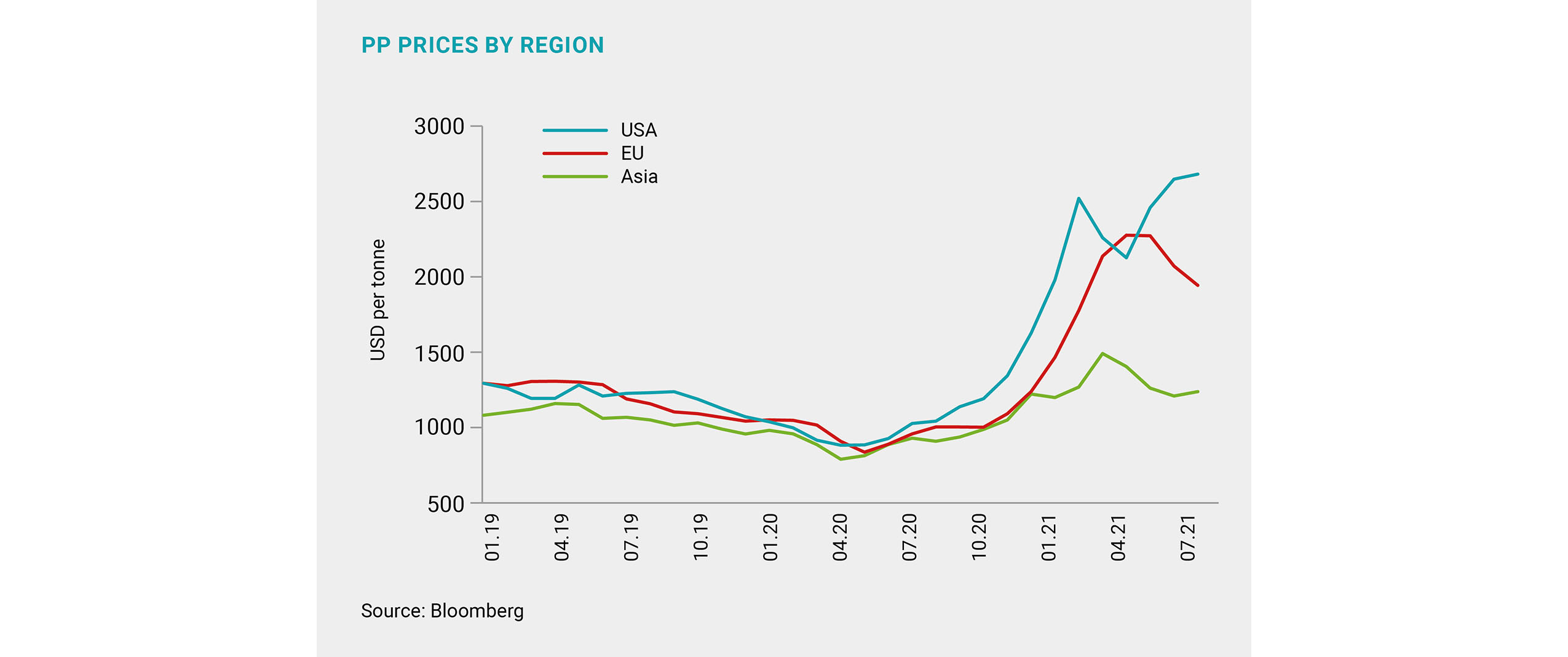

Headlines from Europe mainly relate to lower Q3 prices following production restarts after scheduled and unscheduled shutdowns throughout Q2, which impacted utilisation rates. In September, the price fell to USD 1,655 per tonne, while, for example, in April it exceeded USD 2,200 per tonne. This is on top of the European market continuing to report new launches of plastic recycling projects. For instance, Shell will launch a 60-kt plastic recycling plant in the Netherlands in 2022. Pryme, which supplies raw materials to Shell, plans to launch a 350-kt plastic waste recycling plant in 2024.

PP: bombshell news

Key trends in the polypropylene (PP) market are similar to those in the polyethylene market. Chinese PP production – supported by greenfield projects – is growing in the face of temporary shutdowns and lower utilisation at some PDH (propane dehydrogenation) projects due to declining margins. In the third quarter, China commissioned 1.1 million tonnes of new PP capacity (Jinneng Science and Technology, Liaoyang Petrochemical [PetroChina], and Zhangzhou Gulei Petrochemical). As for the Dual Control policy, analysts do not expect it to have a significant short-term impact on PP supply reduction, something that cannot be said about the increase in raw material costs.

An explosive growth in demand was the key feature of the US PP market – not only in the third quarter, but over 2021 in general. For example, Braskem’s CEO said in an interview that demand for PP in North America for FY2021 is set to increase by 8% year-on-year, stating that the market has reached a unique point of excessive demand and tight supply, yet global arbitrage and logistics are unable to solve this problem in North America. PP demand in the packaging segment has increased due to shifts in consumer demand amid the pandemic. Demand for household goods and food has soared since consumers have been spending more time at home. Demand in the automotive sector is 80% of its pre-COVID level. This situation led to a 22% increase in US PP prices in the third quarter. In September, the PP price reached as high as USD 2,845 per tonne. The ramp-up of the new Braskem plant, launched in late 2020, prevented prices from rising further. The plant planned to supply Europe and Latin America, but instead channelled all of its output to the domestic market. Mrcplast, citing ICIS, also reports that PP imports for 8M 2021 more than doubled year-on-year, with exports down 14%.

BUTADIENE AND RUBBER MARKETS IN ALL REGIONS ARE UNDER PRESSURE FROM DECLINING SALES AND PRODUCTION OF NEW CARS

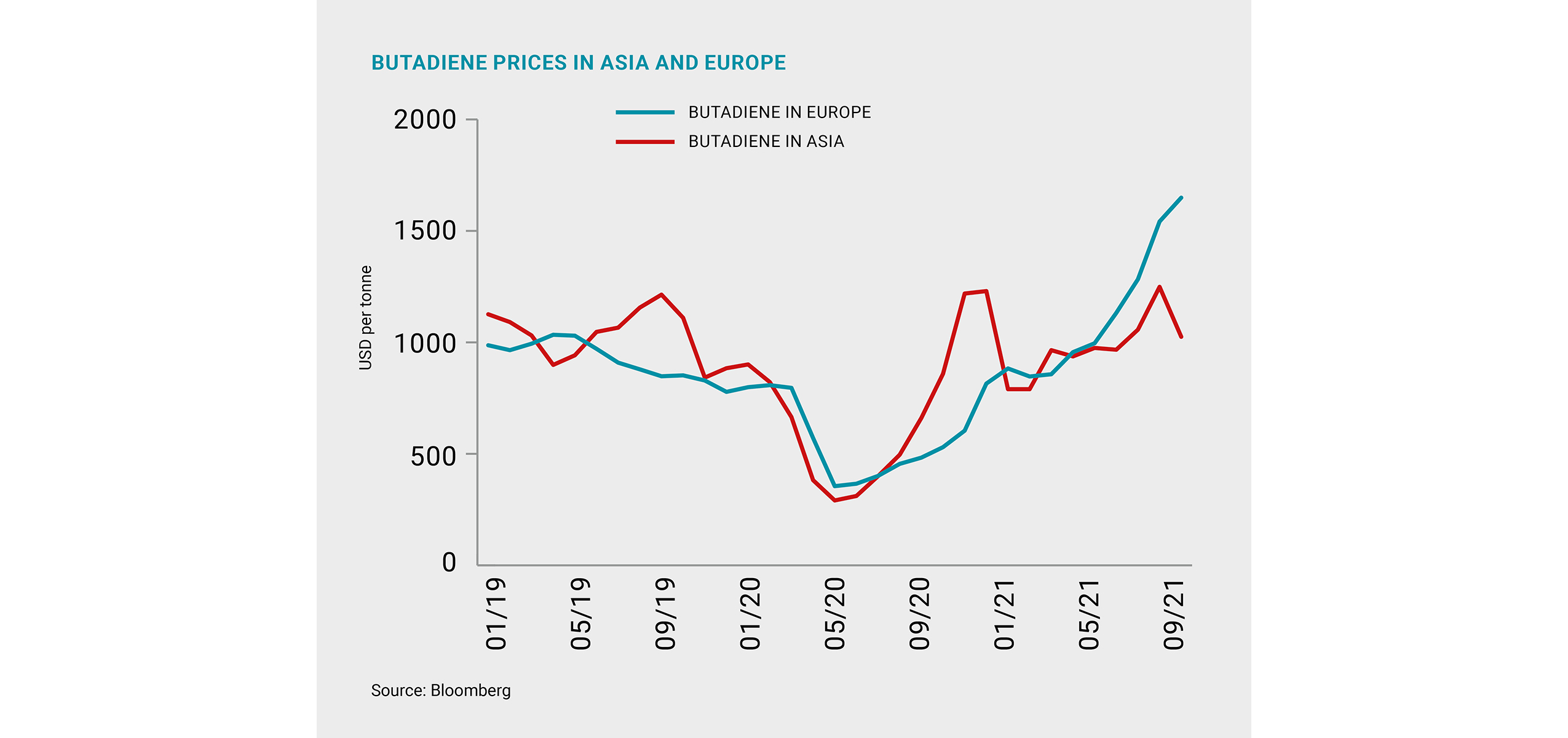

The principal change in Europe was the price correction after its Q2 2021 hike. Prices returned to their standard range following production restarts after scheduled and unscheduled shutdowns. In September, prices dipped to USD 1,885 per tonne after peaking for this year at USD 2,265 per tonne in April.

Rubber: High pressure

In the third quarter, spot prices for styrene-butadiene rubbers decreased in Asia and remained nearly flat in Europe. Price trendlines largely depended on changes in the butadiene price. In Europe, butadiene continued to grow and reached USD 1,650 per tonne in September, while in Asia the price dropped to USD 1,025 per tonne.

Butadiene and rubber markets in all regions are under pressure from declining sales and production of new cars. In the third quarter of 2021, sales in the USA, Europe, and China were cumulatively down 17% year-on-year. The reduction is caused by a number of factors. The most important of these was the shortage of semiconductors on the back of pandemic-related production shutdowns and stronger demand from electronics manufacturers as people were actively buying devices for remote work and study. The rapid economic recovery after the pandemic has exacerbated the problem. Another important reason included the high transport costs for delivery of vehicles. The third was the temporary power outages at Chinese factories following the policy to reduce energy consumption.

Comments (0)