Inflation continues to grow. Petrochemical prices have plateaued. What could be next? Here is what experts from SIBUR’s Investment Planning and IR team have to say about it.

Record macroeconomic performance

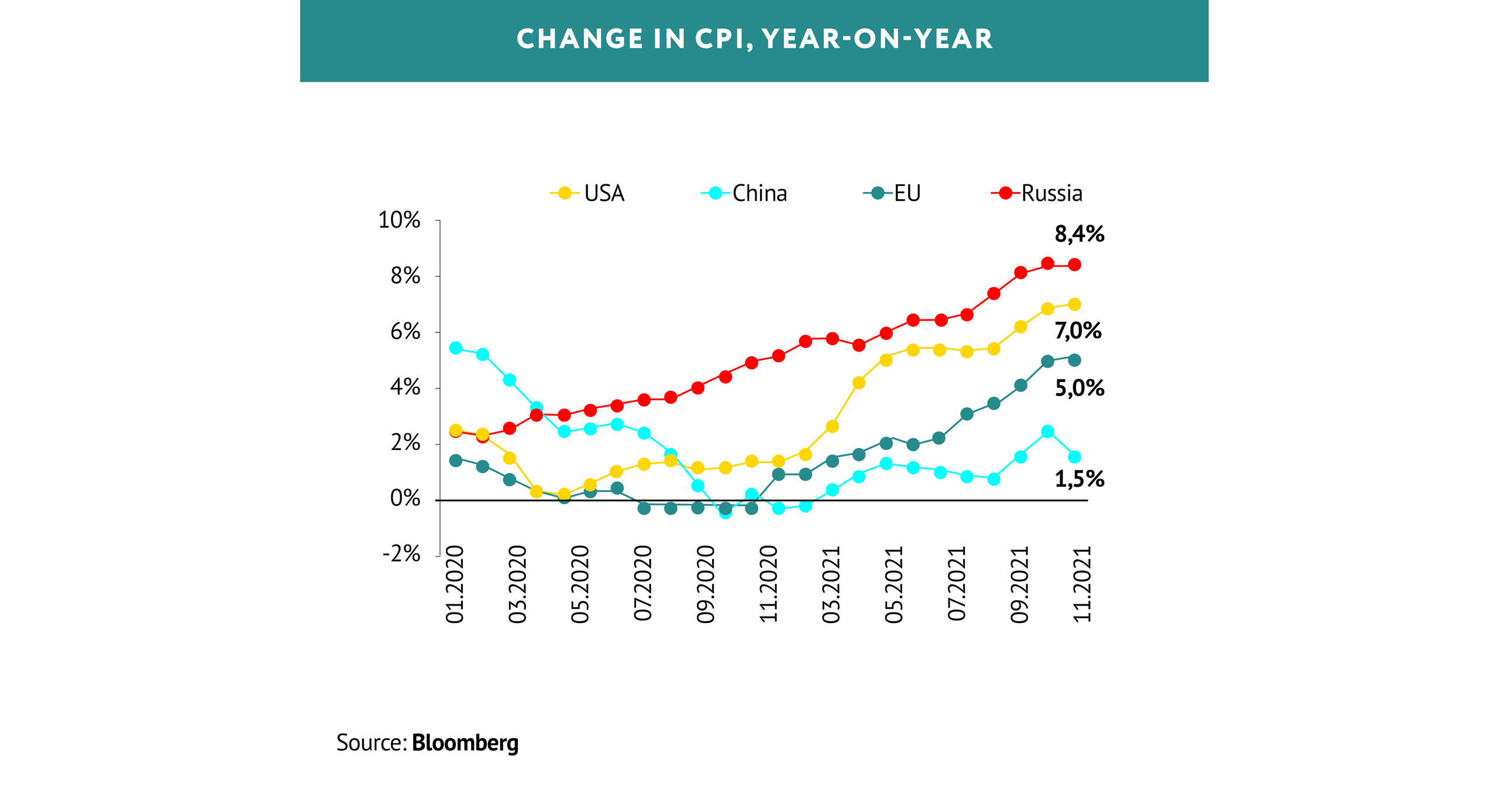

The incessantly rising inflation in advanced economies and most emerging markets remains the hottest item on the economic agenda. The huge central bank stimulus measures of 2020 helped jump-start the economy after the outbreak of the pandemic, but now they have triggered runaway inflation in consumer goods prices. This threatens to slow down economic activity and put the squeeze on debt markets. For example, the price growth in December 2021 in the USA and Europe hit 7% and 5% year-on-year, respectively – the highest levels seen in these regions in three to four decades.

The rise in inflation is largely down to the rising cost of commodities. Global price indices for fuels and metals are up 50% year-on-year, and they can only be kept in check by more active regulation of interest rates. The US Federal Reserve has changed its tune over the past quarter to a tougher one, and markets are expecting stimulus tapering and a run of interest rate hikes. The European Central Bank has so far exercised greater caution, but it has not ruled out a rate hike in 2022, if push comes to shove.

THE RISE IN INFLATION IS LARGELY DOWN TO THE RISING COST OF COMMODITIES

China is moving in the complete opposite direction. The government has started rolling out monetary incentives to tackle the economic slowdown that began in Q4 2021. This drop in economic activity, among other things, was caused by the Dual Control mechanism (something we covered in the previous issue). Now the performance of this tool is currently under review, and the Chinese government plans to shift from controlling energy consumption to curbing carbon emissions.

Oil production: huge potential

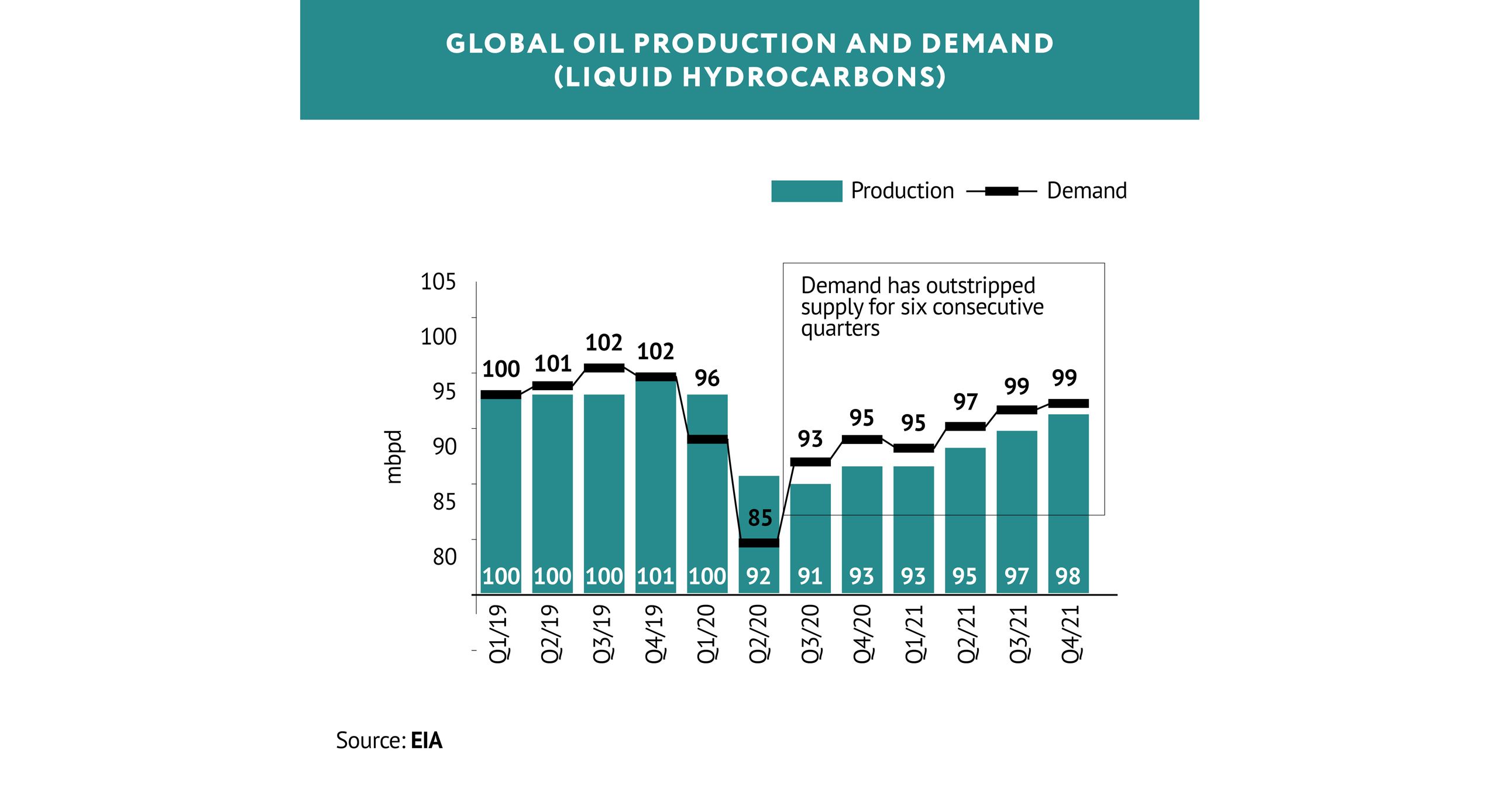

The oil market continued to show stable growth despite concerns over possible drop in demand amid the spread of Omicron. In the fourth quarter, the average Brent price hit USD 80 per barrel, up 8% quarter-on-quarter. Prices were supported by a drop in inventories, which are already at a five-year low. They are falling for the simple reason that demand has outstripped supply for six consecutive quarters.

THE OIL MARKET CONTINUED TO SHOW STABLE GROWTH DESPITE CONCERNS OVER POSSIBLE DROP IN DEMAND AMID THE SPREAD OF OMICRON

The OPEC+ countries have not been fully compliant with agreed oil output targets, with countries including Russia not managing to hit their production quotas, propping up prices. According to S&P Global Platts, OPEC+ countries were 120% compliant in January 2022, the highest level seen since spring 2020; in other words, they under-delivered oil to the market vs their quotas, falling short by around 700 thousand bpd. This lack of supply is mostly driven by a decrease in available capacity, primarily in Saudi Arabia and the UAE. The USA also has room to grow: drilling activity is approaching levels not seen since the beginning of 2020, with oil production in Q4 2021 already hitting 11.5 mbpd, and growing. For context, in Q1 2020 – pre-COVID – US oil production stood at 12.6 mbpd, and with US drilling activity starting to reach these levels, production in the region is only set to follow suit.

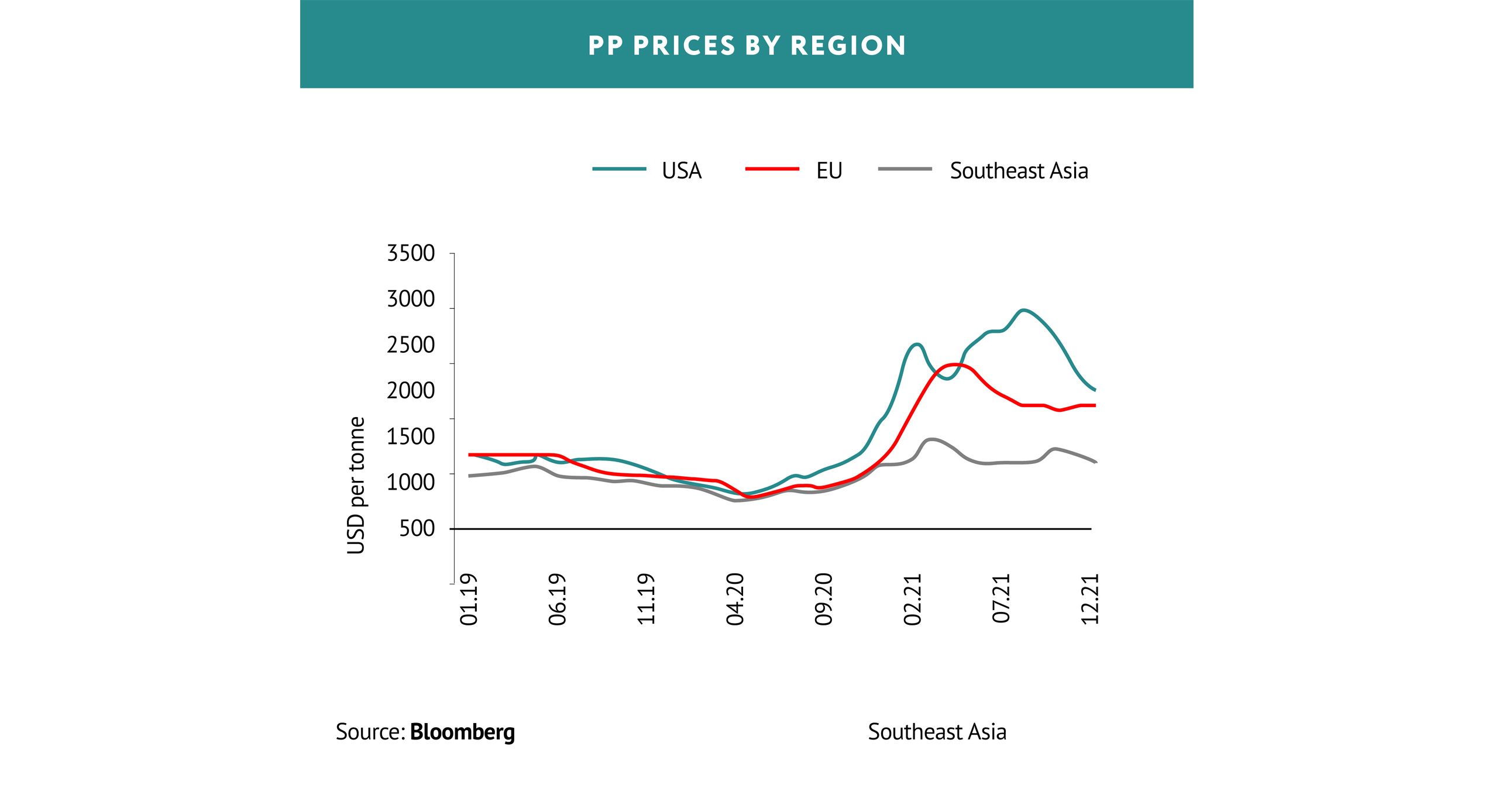

IPEX: Prices have plateaued

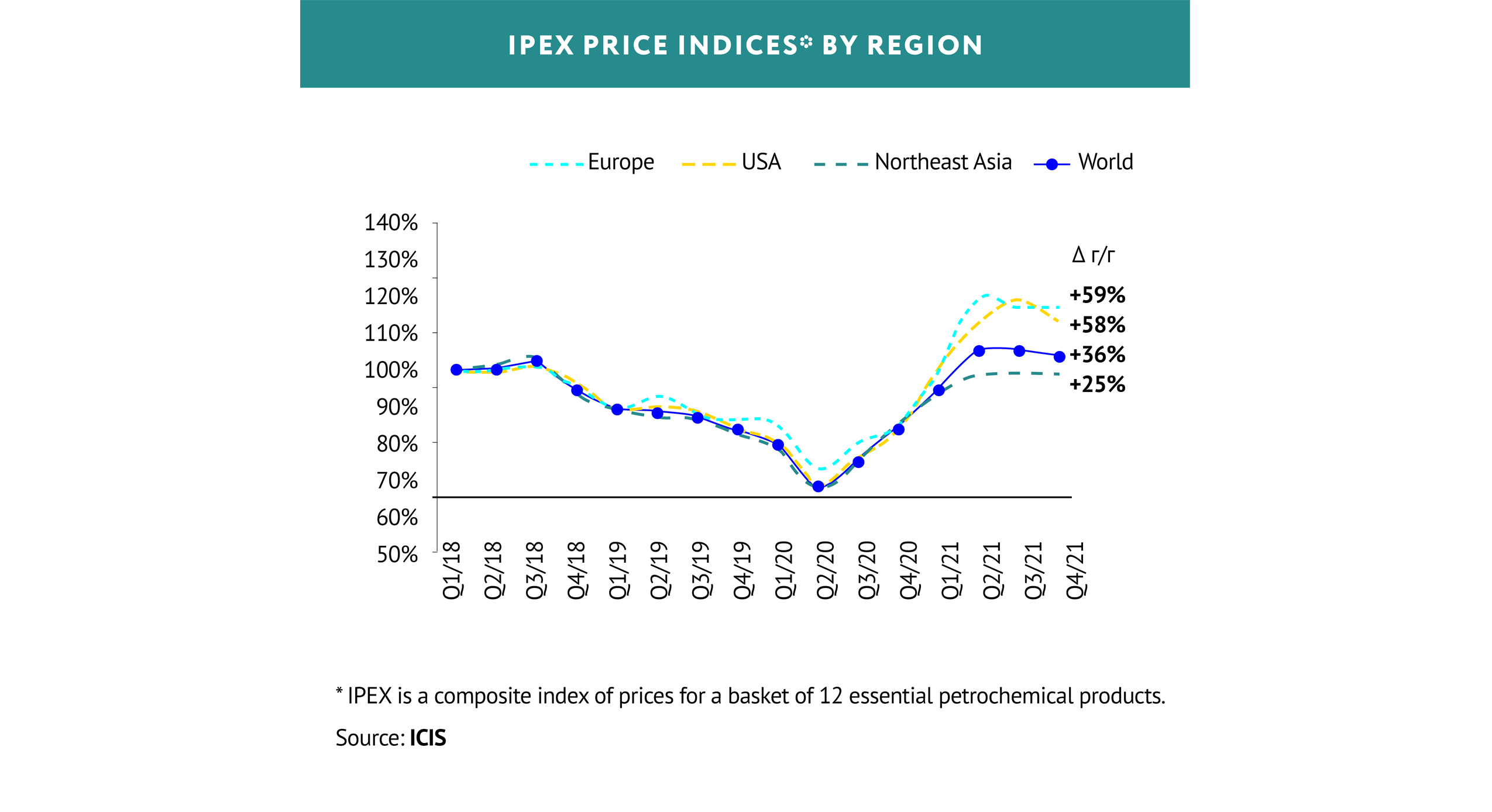

Regional petrochemical prices have plateaued after several back-to-back quarters of strong growth. But there is still a large gap between Asian and Western prices. Prices in the European and North American markets in 2021 skyrocketed by about 60%, while in Asia prices rose by a much more modest 25% (based on the IPEX index).

The price gap between the two regions is held open by high logistics costs. In December, the composite World Container Index stood at USD 9,305 for a 40-foot container, equivalent to USD 376 for a single tonne of polymer. The huge gap in regional prices is also driven by balance sheets. New petrochemical capacity additions continue to come on stream all across Asia, which drives up surplus capacity and brings down prices, especially in China. By the end of 2021, China accounted for 55% of all PE capacity additions and 76% of total PP capacity additions, something that is only set to continue in 2022.

THE PRICE GAP BETWEEN THE TWO REGIONS IS HELD OPEN BY HIGH LOGISTICS COSTS

Last year saw important changes in European environmental regulation: in December 2021, the European Parliament’s Environment Committee proposed an expansion of the carbon border adjustment mechanism (CBAM) to include organic chemicals and polymers. On top of this, they proposed for the mechanism to not just cover direct emissions (Scope 1), but also indirect emissions (Scope 2). The CBAM proposal is currently under consideration, but these measures are highly likely to be adopted this year. It is also worth noting that in 2021, the cost of a permit to emit a single tonne of CO2 in Europe jumped from EUR 40 in January to EUR 85 in December. This rapid increase comes amid growing demand for permits from coal-fired power plants due to comparatively high gas prices.

PE: Demand and production on the up

Production continues to grow in China on the back of new capacity additions coming on stream. According to MRC Plast, China’s total polyethylene output stood at a record 22.4 million tonnes in 2021, an increase of 12% on the previous year. This increase is driven by the output of both previously-launched projects and new ones. Shandong Shouguang Luqing Petrochemical launched two plants with a total capacity of 0.75 million tonnes of PE in November, while December saw Hyundai Chemical introduce 0.5 million tonnes of PE capacity and 0.3 million tonnes of capacity capable of shifting to EVA production. This sharp uptick in production led to a change in trade flows: PE imports to China decreased, while the percentage share of exports increased significantly.

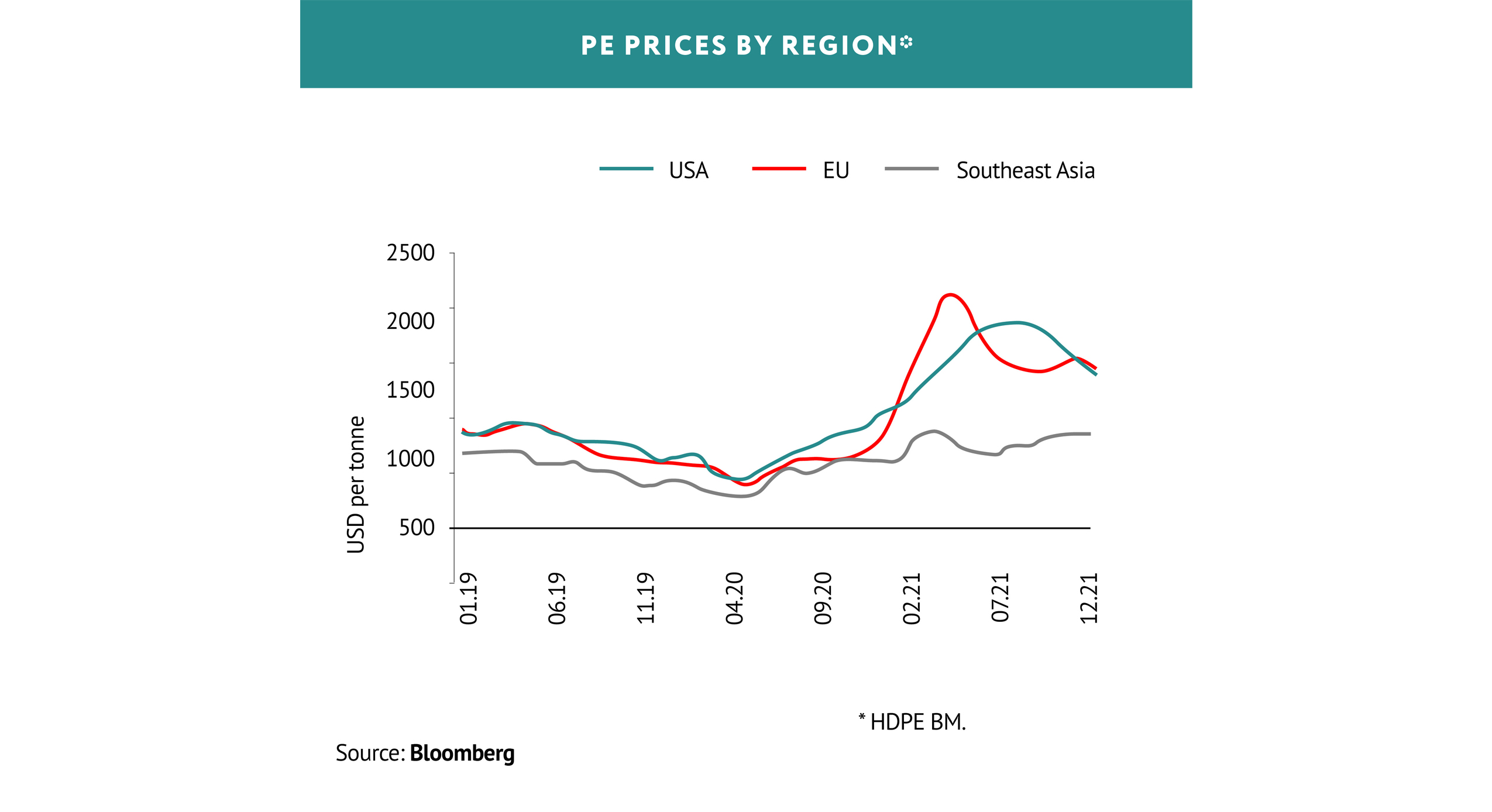

New capacity additions continue coming on stream not only in China but also globally. For example, the second wave of new PE capacity in the USA began in Q4 2021, and will last until 2022-end. The first project to come on stream in the new wave was an ExxonMobil and SABIC facility in Texas, with an annual capacity of 1.3 million tonnes of PE. At the same time, a good deal of capacity that was forced to shut down in autumn due to Hurricane Ida ramped back up again, which led prices to drop to USD 1,500 per tonne by year-end. Prices in Europe and Asia were stable.

THE STATE OF THE PE MARKET IN 2022 WILL BE BROADLY DETERMINED BY DEMAND, WHICH, ALTHOUGH QUITE VOLATILE, HAS BEEN RAPIDLY GROWING OVER THE PAST TWO YEARS

The state of the PE market in 2022 will be broadly determined by demand, which, although quite volatile, has been rapidly growing over the past two years.

PP: Competition is hotting up

The polypropylene (PP) market is showing similar trends. Europe and China are seeing stable prices, while those in the USA are dropping off after peaking in autumn 2021. The high price differential between Europe and Asia has persisted, including due to high logistics costs.

PP production in China grew 14% in 2021 to reach 27.4 million tonnes (according to MRC Plast), which translated to a drop in imports. The growth in PP production in 2022 will lead to increased competition between PP suppliers to China.

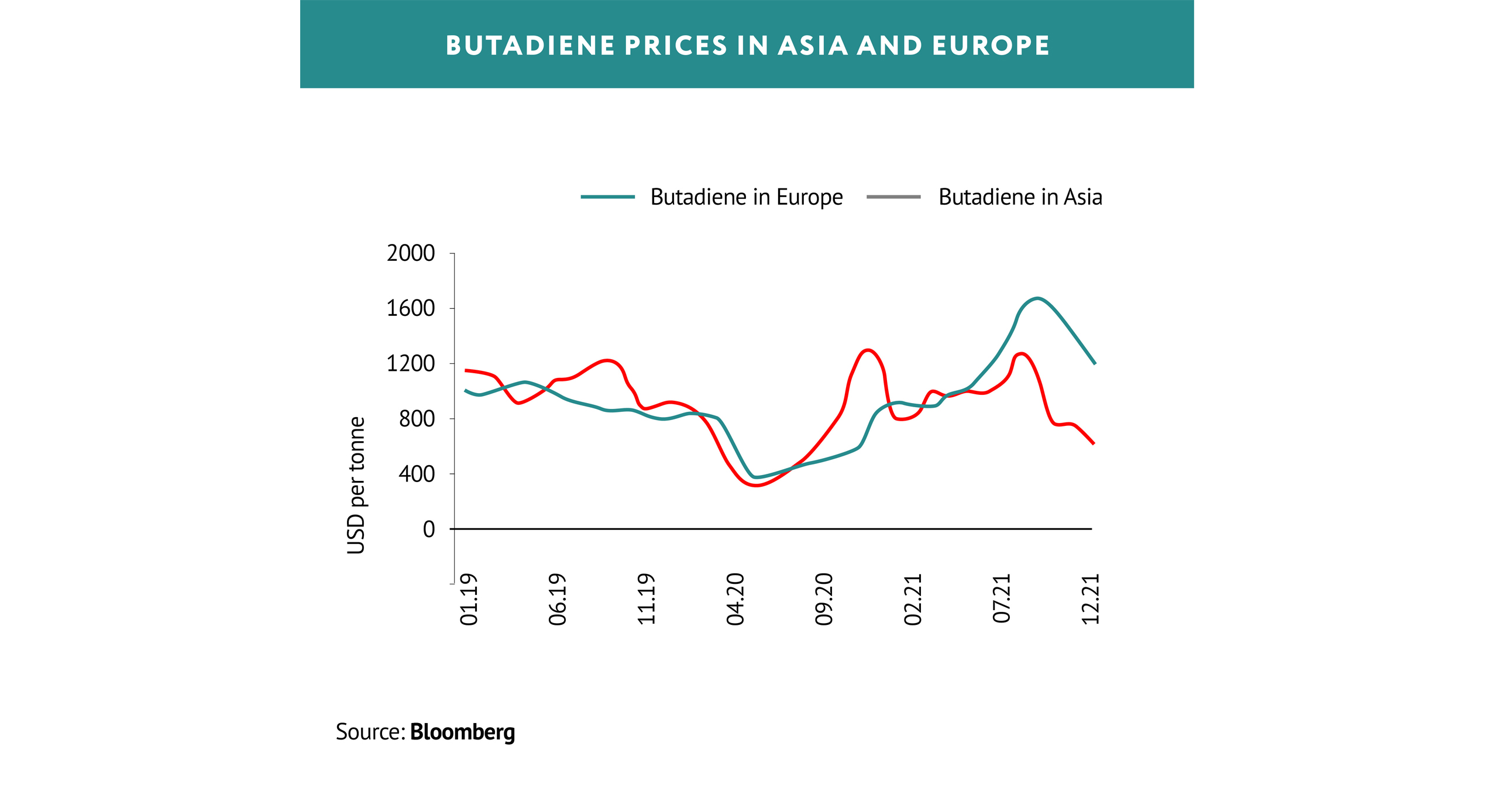

Rubber: A bearish outlook

Sentiment in the Asian synthetic rubber market was negative in the fourth quarter amid low prices for raw materials (butadiene) and weak demand. Total sales of new cars in China, Europe, and the USA for Q4 2021 fell by 14% year-on-year, with carmakers still paralysed by the semiconductor shortage. But this is not all: some electric vehicle manufacturers are reportedly struggling to get hold of batteries.

Looking at butadiene, prices should remain low in the short term. On the one hand, reduced demand for finished products means derivatives producers are losing interest in additional supplies of the material. On the other hand, new crackers coming on stream in Asia are bolstering supply.

Comments (0)